Indonesia is actively pushing forward policies aimed at accelerating the transition to electric vehicles (EVs) and nurturing a flourishing domestic industry. However, to ensure long-term advantages, the government must ensure foreign manufacturers contribute more than just vehicles—they should invest in local employment, supply chains, and technology transfer.

Overview: Indonesia has set ambitious targets of having 2 million electric cars and 12 million electric two-wheelers on the road by 2030. The government’s primary goal is to curb carbon emissions, as the transportation sector remains one of the country’s largest CO2 contributors. Presently, about 11 million cars in Indonesia are responsible for generating over 35 million tons of carbon emissions annually, contributing to 70%–80% of emissions in cities. Indonesia’s strategy goes beyond building a market for EVs—it also aims to capitalize on its vast nickel reserves to become a global leader in EV battery production. The roadmap for growing the EV industry includes three main components: robust battery manufacturing, infrastructure readiness, and making EVs more affordable for consumers.

Policies Driving Growth: In the last two years, Indonesia’s government has introduced several policies designed to stimulate EV adoption and industry growth, benefiting both local and foreign manufacturers. But will these policies pave the way for sustainable growth, or will they only result in a short-term boom in EV numbers?

Key Incentives for EV Adoption:

- VAT Reduction for Domestic Manufacturers:

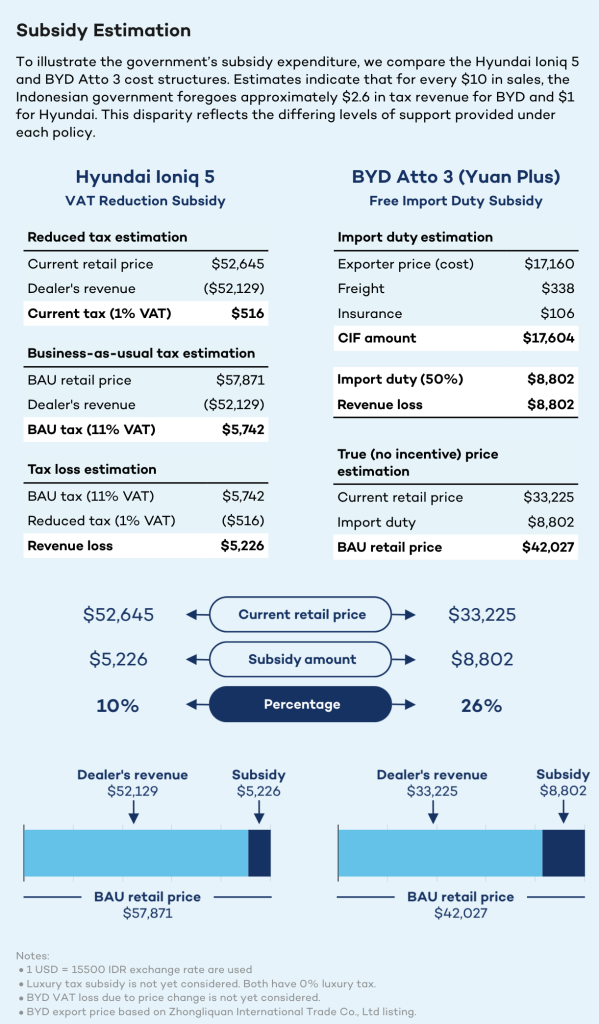

Starting in April 2023 and continuing in 2024, a major incentive has been the reduction of value-added tax (VAT) for EVs with local manufacturing facilities, dropping from 11% to just 1% for vehicles meeting a 40% local content requirement. This reduction has made EVs more affordable for consumers, with brands like Hyundai and Wuling benefiting significantly. The policy has led to a marked 104.13% growth in EV interest in the second quarter of 2024, although EVs still make up a small fraction (2.92%) of total car sales. - Zero Import Duty for Foreign Manufacturers:

A new incentive for foreign manufacturers is the 0% import duty on completely built-up (CBU) and completely knocked-down (CKD) EVs, provided they establish domestic factories by 2026. Manufacturers like BYD are participating, but this has led to an imbalance in subsidies, with BYD, for example, receiving a larger subsidy compared to Hyundai.

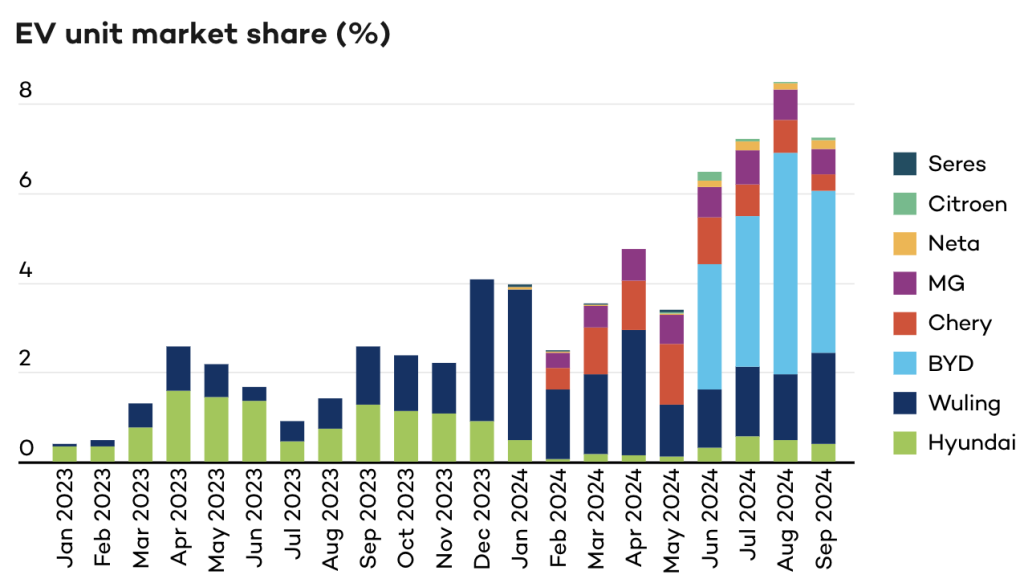

Market Reactions: The market has responded favorably to these policies. After the VAT reduction, new entrants such as Chery, Neta, MG, and Seres quickly established factories in Indonesia. Additionally, the import policy introduced in May 2024 triggered a significant increase in sales of foreign brands like BYD and Citroen. BYD alone accounted for half of total EV sales, highlighting how quickly imported EVs are gaining traction. However, this shift has caused some domestic manufacturers like Hyundai to experience a sharp drop in sales, signaling the dominance of foreign imports in the market.

Challenges for Domestic Manufacturers: Indonesia’s EV ecosystem requires more than just assembly plants—it necessitates substantial investments in upstream components such as battery manufacturing and charging infrastructure. Hyundai has invested significantly in this, owning 18% of public EV charging units. Yet, the government’s import policies have led Hyundai to restrict its charging stations to its own EVs, which has reduced public access to charging infrastructure even as the number of EVs grows. This decision highlights a downside to the import subsidies, as it discourages further investment from established players who face stiffer competition from foreign entrants.

Risks and Concerns:

- Short Market Evaluation Window:

The two-year period for foreign manufacturers to assess the market and establish local operations may be too brief, possibly deterring potential entrants who require more time for evaluation and capacity building. This tight timeline could lead to market exclusivity for early entrants like BYD, which might undermine competition. - Minimal Local Content (TKDN):

For sustainable growth, a significant local content in manufacturing is required. Currently, the domestic content threshold is 40%, primarily fulfilled by final assembly. The target is to increase this to 60% by 2026, but manufacturers’ limited investment in local component production could undermine this goal. The policy of allowing duty-free imports for CBUs conflicts with efforts to build a robust domestic EV industry. - Over Subsidization:

Generous subsidies for foreign manufacturers, such as BYD, could create an unfair advantage for them over local producers like Hyundai. This disparity is exacerbated by the possibility that BYD’s vehicles already benefit from subsidies in China, leading to additional competitive pressure on local manufacturers.

Looking Ahead: Indonesia’s incentive policies have demonstrated a strong commitment to increasing EV adoption. However, several risks remain that could hinder the long-term success of the strategy. The conflicting incentives between promoting short-term imports and fostering local production could destabilize the EV ecosystem and prevent the achievement of long-term industrial goals. If the government continues offering substantial subsidies to foreign manufacturers without ensuring robust local production, the benefits of these policies may not justify their costs. Only time will tell if Indonesia can create a self-sustaining EV industry with a thriving local supply chain.

Source:

PT Hyundai Mobil Indonesia price list